How to think and manage like the top venture capitalists who receive 13x or higher revenue streams for their investors.

In business, there is a lot of wisdom — good and bad — but few facts. However, of the things we do know, the indisputability that inventions and innovation drive economic competitiveness is key. Likewise, it is vital to note that the venture capital industry plays a key role in fueling the startup ecosystem, which is the driving force for innovation. Starting from only a few dozen venture capital firms in the 1970s, Preqin now reports that venture capital is a $1.9 trillion industry that accounts for 20% of private market Assets Under Management (AUM) globally, with fundraising growing at 10% per year.

According to Statista, venture capital investments in the US alone have grown from $22 billion in 2009 to $130 billion in 2020. Moreover, globally, venture capital funds’ investment strategies recorded the best performance among all private capital investment strategies for several years in a row and in the first quarter of 2021, according to PitchBook’s latest benchmarks, with an IRR of 20%.

The other trend to observe is that the lifetime of existing and running businesses is shrinking. The idea is this: Companies don’t need to be startups to grow like companies within the venture capitalist portfolio. In fact, there are several advantages to holding well-established running companies — no matter their size — in achieving a performance that is among the top venture capital firms. In this article, we examine these investment strategies and the lessons that can be learned from them. We will also take a look at how venture capitalists invest, how venture capitalist firms are run, and lastly, how a successful portfolio management strategy can be adopted in managing and growing businesses of all sizes — in any sector — by investing a tiny portion of your income into a smart portfolio of winning bets.

How Do Venture Capitalists Invest?

According to William Sahlman at Harvard Business School, the performance of the trillion-dollar venture capital industry can be said to follow the Pareto Principle. If you’re not familiar with Pareto Principle — often referred to as the 80/20 rule — it is when roughly 80% of consequences stem from 20% of causes. While this is not a formal mathematical equation but rather an occurrence that can be observed with statistical significance across areas such as finance, time management, and sports. Although the principle applies to almost every industry imaginable, it is most commonly used in business and economics.

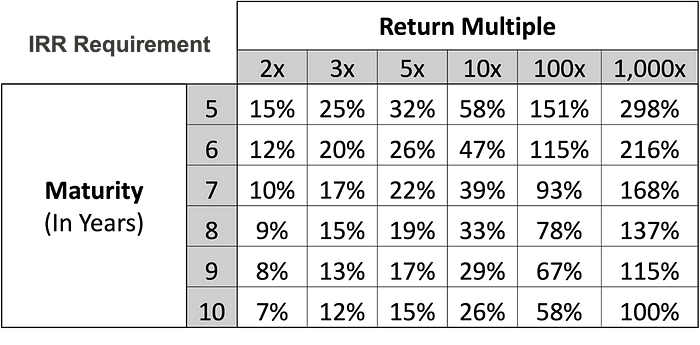

By applying the 80/20 rule to the AUM of venture capital funds, 20% of the AUM would eventually account for 80% of returns. Now, if you then recursively apply the 80/20 Rule to the top 20% of AUM, Prequin data indicates that you get an average IRR of 60% overall for these funds and an average of a 1,000x return for one in every five investments in these top-performing funds.

Because one in five deals needs to be a big win, the industry rule of thumb has been to seek out deals that return 10x in 5 years — or what is commonly referred to as the hurdle rate of 60% IRR for prospective investments.

If these numbers are confusing, the main takeaway here is that, despite asymmetric information, the top venture capital firms are still able to achieve strong returns by betting intuitively on the right horses.

Venture capitalists are credited for enabling technologies that reshape industries and transform lives, providing promising startups and entrepreneurs with the capital they need to grow.

While the overwhelming majority of their investments don’t pan out, many ideas that may have seemed absurd at first have turned into billion-dollar wins and changed our lives. Of course, there is no surefire formula, but the boldest, most ambitious bets did end up, in many cases, being their biggest winners.

How Businesses Are Run

Let us compare venture capital investments and portfolio management to how businesses, in general, are managed. It is not obvious to see the similarity, but that is primarily the core of the problem being discussed here.

For the purpose of this discussion, we can define a business or a company as a simple entity that maintains its livelihood from a stream of revenues, with revenues being the cost of a product or service multiplied by units sold.

Now, let us consider the trends — both historical and in terms of future prospects — of the difference between, on the one hand, the stream of revenues that are being sold to a client or customer who pays for the products or services at an agreed-upon price and, on the other hand, the cost and expenses of a company as an indicator of that company’s health. Furthermore, for this article’s purpose, I will focus on examples from publicly traded companies and assume the stock price or market cap is an indicator of how well the company is doing. Keep in mind that the analogy can be applied to any size and any type of company. I chose public companies so that you can look them up online if you want to see how this analogy applies to your industry.

Now, let us further examine the difference between companies that have failed due to declining revenues and those thriving at the time of publication.

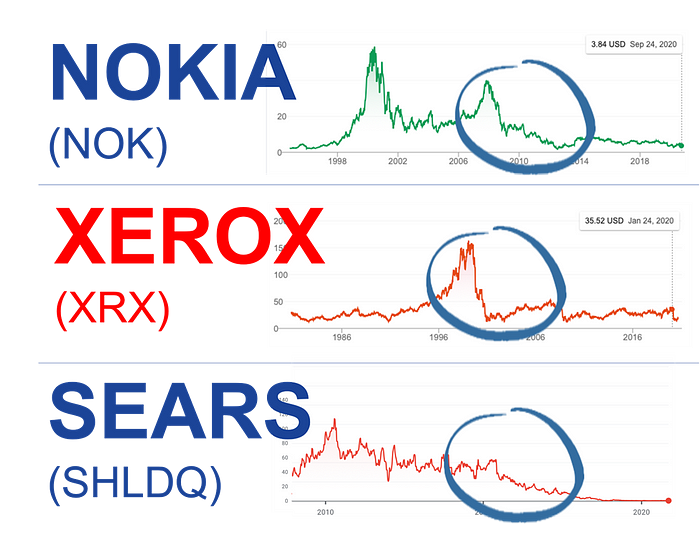

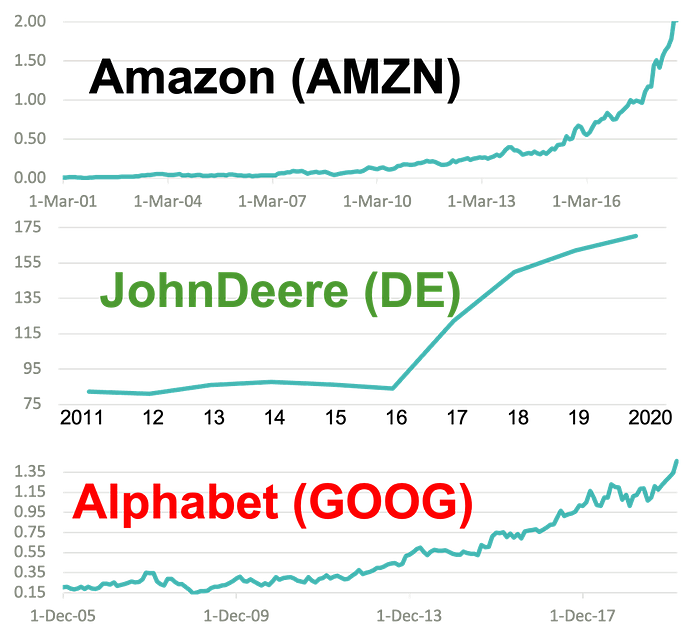

For example, consider once-iconic, now-failed companies such as Nokia, Radioshack, Kodak, JCPenny, Compaq, Blockbuster, Sears, and Blackberry, compared to companies that have seen a consistent increase in their prices — regardless of overall market conditions and black swan events — such as JohnDeere, Lowes, Amazon, and Google. The key distinction between these two categories of companies is in the strategy they adopt to grow their revenue streams.

Suppose you were to conduct in-depth research on the company examples I provided. In that case, you might determine that the companies that have sustained consistent growth and weathered market turmoil were those that placed bets on several experiments over time and continued to do so to this very day. The companies that have shown consistent growth over the last two decades are the ones that have been able to continuously experiment and make bets on new revenue streams that I will refer to here as ‘experiments’ or ‘options.’

Successful companies like Lowes often have an innovation lab designed to churn out new experiments on a regular basis. Google has been going hard at diversifying their revenue streams away from Internet search tools ever since they started, launching and testing numerous ideas such as Google Voice, Plus, Wave, Docs, Gmail, Glass, etc.; many such ideas failed — the same is true of Amazon with Destination, Local, Wallet, Importer, Fire Phone, Kindle, AWS, etc.

You may be thinking when I cite these examples: “Well, Sam, these are huge companies with deep pockets — that’s why it worked for them.” However, this is not entirely true, as companies like Lowe’s and JohnDeere were worth a mere 1/10th of their value just a decade earlier (i.e., less than the $20 billion market cap).

In addition, consider the other side of the equation — the companies that have failed over time. These companies rarely placed any bets or experiments. From their business model to their product portfolio, these failed companies only decided to experiment and place bets on new ventures when it was already too late. And, what’s worse is that when they did put a bet, they did it by introducing nothing new. Instead, they copied the competition that was already way ahead of them. For example, Blackberry went into the Android space, and Sears went into the online space long after their competitors had already gotten way ahead of them.

Taking this claim further, I can cite several examples from our firm’s direct engagement experience with smaller businesses that grew from Mom & Pop, dying, and stagnant organizations to a 100x value in three years or less by applying experiments and an options’ strategy without the need for huge external resources or loans. We did this by allocating a very small portion of these businesses’ ongoing income stream into tiny sequential bets. If one of the bets showed promise, then a greater investment was allocated, and external financing was only sought after an experiment had proven profitable and needed geographical scaling to achieve 10x or more returns on investment.

We have worked with companies operating in a range of industries, from food manufacturing to 3D printing, and — in every single case — the bets succeeded in one in three experiments with an average of 56% IRR. This is compared against one in five at an average IRR of 20% for venture capital firms. The main reason for this is that the business owners had all (or more than enough of) their skin in the game, which made it more of a high-stakes game. In fact, you’d probably agree that it’s much easier to get 100x return on a company worth $1 million than on a company worth $10 billion, given the scale of return this proportion would require.

How a Portfolio Management Strategy Applies to any Business

For simplicity’s sake, the idea of venture capital portfolio management is, as we discussed earlier, that the more bets you make on experiments in viable goods or services, the more likely your chances of hitting the jackpot are because a portfolio with dozens of options is less likely to fail than a portfolio with a single option. Now, you can view your single option as your current business, and if you want to add bets to your portfolio, you need to add options. But what are the options and experiments in your business? Many businesses have hidden and buried options under existing operations, but they have no way to unveil them. Other options and experiments may need to be developed from scratch, but, to make it simple, we can go along with options that fall within the existing core competencies of the running business.

Optionalities exist in even the smallest of companies. They can be identified in one of the six dimensions shown below, and while non-exhaustive, I’m hoping that these categories can provide guidance on how to reconsider your current business revenue streams as options for winning portfolio management. However, they need to be assessed on an ongoing basis to unveil new options for experiments.

- Product or Service: An obvious option is your main revenue stream, which results from products or services that you sell. Examples of experiments here include bundles, side-products and upsells, rebranded goods, white labels, and franchises. In addition, you can look into converting your product into a service, e.g., PaaS off your service, into a product such as software.

- Geography: Most of your revenue will come from a specific area, such as a district, country, region, continent, etc. In which case, you can leverage geographic options in one of two ways, depending on your business. For example, if you are present in multiple locations, you can add an additional product or service to your existing product/service in these geographic areas. This addition can come from your current core portfolio, or — by adding a complementary product or service through partnership, you can target different niches within the same geographic area and expand beyond your existing area either through local partnerships, licensing, or franchise.

- Channel: If you are a business that relies on distribution or sales as your core revenue stream, optionality can come from diversifying these channels into digital or web sales. Experimental options here could range from channel partnership, OEMs, affiliates, retail, wholesalers, and direct-to-consumer (D2C) channels. You can convert your assets into services for recurrent fees — e.g., warehousing and distribution capabilities — or the opposite: Lease the assets or refocus on channel and supply chain as core capabilities.

- Core Capabilities: If your business’s strength and value proposition are its core capabilities, adding options can take the form of a proprietary IP, certifications, licensing, or proprietary soft- or hardware, patents, branding — or the opposite: You can leverage manufacturing capabilities to produce white label products, for example. If you’re in service, you can partner with larger companies as a subcontractor.

- Customer Segment: Every business targets specific customer segments. The possibilities for experiments with customer segments are endless. Establish what these possibilities currently are and then iteratively consider what adding additional segments to your portfolio would mean to your offer. If you are serving corporate customers, can you add the government? If you serve pet owners, can you add vets and pet trainers? You can also consider expanding your offer: For example, can you add new products or services to your existing offer without cannibalizing your sales? If so, what would those be?

These are just a few examples of possible options, but you can go deeper and apply low-cost emerging technologies to change your business model by offering the same product or service differently or applying what we call ‘business model hacks.’

Business model hacks vary from obvious examples — such as how Airbnb created a market from existing apartments and Uber transformed public transportation — to lesser-known examples, such as Kaeser Compressors that offers Air-as-a-Service and Appear Here (the Airbnb for retail space). But business model hacks don’t have to be costly to create. They could be simple options, such as scaling your limited brick and mortar business into a branded D2C brand, or more complex. For instance, if you own a chain of restaurants, you are sitting on an underutilized pool of expensive assets for almost half the time. You can potentially utilize those assets for revenue and convert your kitchens into distributed facilities for ready-to-eat food production for your own brands or other brands.

Why and How to Apply this to any Running Business

All businesses can benefit from this strategy — be they large and established enterprises or small startups taking their first steps in diversifying. All businesses need experiments and options. These ensure economic endurance and allow companies to attain sustainable nonlinear growth. This is not only how venture capitalists manage their portfolios but also how business owners should manage their businesses. Unlike venture capital investments in startups, existing and running businesses do not need shareholder dilution of their existing businesses to run experiments and options. You don’t have the risk of asymmetric information that venture capitalists take when they invest in startups.

If you enjoyed reading this piece, don’t miss out on my other articles:

A Cancer Tale that Altered the Course of My Life

Why Today’s Management Practices Are Out Of Touch With Reality

References

Mayers, J. (2021). VC fund performance continues to stand out in early 2021 returns. Pitchbook. Retrieved from https://pitchbook.com/news/articles/vc-fund-performance-2021-returns.

McCahery, J. & Renneboog, L. (2003). Venture capital contracting and the valuation of high-technology firms. Oxford: Oxford University Press.

Ramsinghani, M. (2014). The business of venture capital: insights from leading practitioners on the art of raising a fund, deal structuring, value creation, and exit strategies. Hoboken, New Jersey: Wiley Press.

Reeves, M. (2015). Die Another Day: What Leaders Can Do About the Shrinking Life Expectancy of Corporations. BCG. Retrieved from https://www.bcg.com/publications/2015/strategy-die-another-day-what-leaders-can-do-about-the-shrinking-life-expectancy-of-corporations.

Top performing venture capital funds. (2018). Prequin. Retrieved from https://docs.preqin.com/reports/Preqin-Top-Performing-Venture-Capital-Funds-March-2018.pdf

Value of venture capitalism investment in the United States from 1995 to 2020. (2022). Statista. Retrieved from https://www.statista.com/statistics/277501/venture-capital-amount-invested-in-the-united-states-since-1995/