How and when benchmarking and best practices can be detrimental to businesses

Picture this scenario. You come to work one day, and you find an anonymous file containing the most secret details of your closest competitor. The file includes everything you could’ve imagined or wanted to know about your competitor, including their trade secrets, key people, cost structure, pricing strategy, strategic plans, financial positions, etc. Now ask yourself this question: Can you use this information to improve your business performance?

Before you answer, let’s take this scenario one step further and picture a second scenario in which, hypothetically, you not only have all the intelligence about your competitor at your fingertips but also gain access to the company’s entire resources and have at your disposal: The exact same staff, IPs, markets, customers, production lines, and so on… Now, ask yourself again the same question: Can these resources improve your business performance? If so, by how much?

Military experts will tell you that intelligence and information about your enemy are everything in a battle if you think of the analogy to wars. So, intuitively, the same must be true in business, right?

As it turns out, the answer to this question is not that simple. But one thing is certain: Over the past decade, numerous surveys of companies that had access to resources in either scenario found that across the board, the average improvement in performance turned out to be negative within three years of having such access. Don’t worry, we’ll explain in a minute.

Before we get into it, let us introduce and define several concepts from systems thinking, behavioral economics, and management tools that you may or may not be familiar with. This is to give you the background you need to understand the logic.

In any case, whether you’re familiar with this exciting new field of complex systems and behavioral science and their implications on the enterprise and business practices, or happen to lead a business or an organization of any kind, the time for you to add systems thinking to your business suite of tools and leadership skills is now.

Let’s face it; we live in an increasingly complex and competitive world where we swim in a sea of data and where “winner-takes-all” is the new benchmark for success. But today’s management practices have not kept pace with modern organizations and these growing complexities in business.

Advancements in complex systems are reshaping organizations at an unprecedented pace. As a result, organizations and leaders adopting systems thinking in their day-to-day business management are experiencing a metamorphosis of their business models, leading to lasting benefits.

You see, traditional methods and today’s management science were developed during the Industrial Revolution almost a century ago. They were great for that era and got us where we are today. These tools and methods have been polished, rebranded, and slapped with new buzzwords to make them appear modern. However, if you scratch the surface, you’ll quickly realize that today’s management tools and best practices are mostly obsolete and are ill-suited for tackling most business challenges that modern enterprises are currently facing.

Let’s go back to our main topic and examine the second scenario, where all resources would be at your fingertips.

How do companies gain access to competitors’ resources?

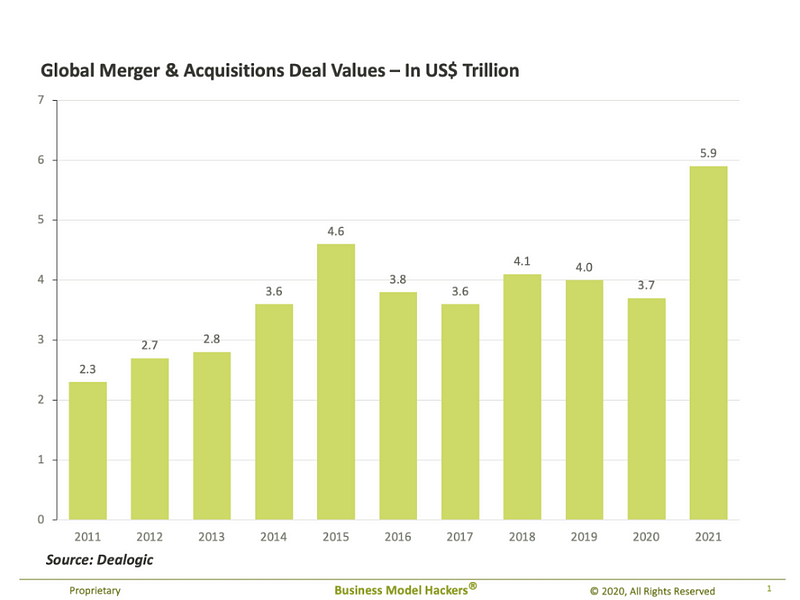

The answer is simple, how about if you were to acquire or merge with your competitor? Think about it. What’s the single driver and motivator for M&As? If you answered Synergies, you’re spot-on. Whether driven by scope or scale objectives, mergers and acquisitions are common strategies adopted by companies looking to improve a company’s performance that is much greater than organic or status quo performance by merging or acquiring resources of other companies. If your acquisition is not somehow monopolizing the market, which is the case for 99% of such transactions, the FTC or the relevant authorities are not likely to block your merger. That’s why this strategy remains a growing trend among companies, spending over three trillion dollars in mergers and acquisitions every year and a whopping six trillion dollars in M&A transactions in 2021 alone.

But what are synergies?

Synergies are arguably the most important indicators of an organization’s performance. The word has it in its Greek roots, which means “working together.”

In complex systems, they are defined as the relationship between at least two parts in a system where the resulting interaction generates either more or less than the raw sum of its parts. There are positive and negative synergies:

- Negative synergies happen if an interaction between elements — in this case, employees in an organization — is less than the sum of its parts. Or where 1+1 < 2

- Positive Synergies arise from positive feedback loops between elements and when such interaction leads to more than the sum of its parts. 1+1 > 2

Examples of positive synergies in nature are how flowers and bees interact to pollinate flowers and produce honey. In business, members of a diverse team or teams interact to create or introduce new winning products to the market.

Around $40 trillion worth of M&A transactions took place over the past decade, with companies looking to monetize possible synergies. So how did these mergers turn out?

Every year, several studies on tens of thousands of deals are conducted by reputable firms to measure the impact of a potential M&A on a company’s performance. In addition, they monitor the deals over a decade trailing. These results vary slightly, but the conclusion is always the same. In most M&A transactions, approximately two out of three mergers lead to negative synergies and value destruction.

What about those that succeed? Well, the benefits for successful mergers and acquisitions are usually a minimal improvement in performance after the deal is concluded and after post-merger integrations, which usually occurs after the second or third year.

In other words, your three-year payback after you factor in 5–10% transaction fees and the effort and cost of post-merger integration, your payback is likely to be 1x or less. But, you may be thinking, what about after three years? And the answer to that question is a whole different topic on forecasts and strategic planning. But what’s important for you to know here is that anything beyond a few years can be anyone’s guess, and those who strongly believe in the accuracy of four+ years forecasts in such a complex world and an ever-changing business climate are likely falling for Prospect Theory biases. Hold that thought for a minute; we’re getting into it shortly.

With these numbers and payouts, how do you feel about that second scenario if you were considering synergies as your goal from acquisition, considering the amount of effort that goes into such transactions? Was this the performance you had in mind when we asked you that question initially?

That said, there are cases where M&As can lead to benefits beyond the synergies to the acquirer, such as optionalities-based and purely scope-driven acquisitions in the process of portfolio management, for example, the case of Facebook’s acquisitions of Instagram or Oculus or Amazon’s acquisitions of Ring, twitch, and Zoox. This is when the acquirer adds an entirely new business line, mainly with the strategic objective as a bet on optionalities, which is a huge topic that we’ll touch on briefly here, but that’s not where the majority of four trillion dollars of annual acquisition are typically invested.

Before moving to the first scenario, most M&A studies go beyond just assessing payoff and value; they’re conducted to determine why mergers fail, such as these recent ones conducted by BCG and Bain. Among the cited leading causes for post-merger integration failures are “cultural fit” and “low synergies.” And here’s the problem. Many companies proceed with M&As even when they internally have huge gaps in synergies internally. There was no easy way to effectively determine and measure synergies for pre-and post-merger. Suppose you happen to be in a post-merger or acquisition situation or seriously considering an acquisition and are interested in such a tool. In that case, we are here to help you get it done quickly and effectively. Please ping us in the chat or on our website, as you won’t find this tool elsewhere.

But what’s most interesting is the root cause of why this happens, such as the one conducted by Bain and Company, which found that “Overestimated synergies from combining the companies” as the leading root cause of failure in 55% of surveyed companies. This takes us to the first scenario.

What is benchmarking?

Now let’s go back to the first question we asked at the beginning. What would happen to your performance if you had all the intelligence you wanted about your competitors? In this case, you are in a scenario where you’re not taking an acquisition risk. So, what do you think is a fair estimate of your performance improvement?

Hold that thought for a minute.

Everyone in a management or leadership role tends to look at what worked for others and only then copy or adopt it. So we run case studies, develop lessons learned, conduct benchmarking, hire like-minded individuals, steal employees from our competitors, bring in subject matter experts, etc. Then, we hope that we will outperform our competitors and apply best practices others have developed and refined, so we don’t have to.

But what do you think is the outcome of this management approach in most scenarios?

Let’s consider a highly popular management tool such as benchmarking, another name for having intelligence about competitors. As you know, many research companies and consulting firms specialize in benchmarking or legal information sharing about specific industries. As a matter of fact, many companies willingly, even eagerly, participate in sharing such information so that they, in turn, can pay consulting companies to have access to such industry benchmarks.

When benchmarking, we set the performance bar at a level that inadvertently but automatically puts a cap on our performance goals. So, as a result, most of the time, we end up focusing on small gains and minor improvements in our organizations that hold us back from achieving extraordinary or transformational outcomes. But, of course, that is without factoring in the effort and the opportunity cost to the equation.

It’s in our nature as humans to be risk-averse but, at the same time, overconfident, which makes up a dangerous combination. Let us explain further. These findings from behavioral economics are based on experimental research conducted by Daniel Kahneman, referred to as Prospect Theory, for which he was awarded the Nobel Prize in 2002. Kahneman explained it in detail in his best-selling book Thinking Fast and Slow, where he compressed his lifelong research on behavioral economics. Prospect theory is a paradox, and I consider Kahneman’s findings nothing short of extraordinary in many respects. They have far-reaching implications in managerial decision-making and decisions taken by leaders in financial markets, public policy, wars, global trade, and more.

Here, the focus is on one relevant angle, which is the fact that not only did Kahneman’s research show how risk-averse we humans are, but it went further and quantified by how much. And, as it turns out, people hate losing by two to three times more than they like winning. Therefore, it’s not surprising that we are risk-averse when trying out new things. That’s why very few companies dare to venture out into the unknown, except maybe for people like Elon Musk, venture capitalists, and companies with deep pockets who initially pay a hefty price before it pays off for them in the long term. But combining that with the findings that people are overconfident and optimistic, you get a dangerous formula. When Kahneman was once asked which cognitive bias he would eliminate if he had a magic wand, his answer was ‘overconfidence.’

You can understand why Kahneman said that if you consider the M&A example we described earlier. You can easily attribute one of the leading causes of M&A failure, “Overestimated synergies from combining the companies,” to the human nature of overconfidence and optimism.

On the other hand, overconfidence and optimism are the leading causes of entrepreneurial activity. For example, if entrepreneurs considered the statistics of startup failure rates, which exceed 90%, and factor in the payout, no startup would ever come to fruition, and entrepreneurs would never start new companies.

But where the real problem lies is when overconfidence and risk aversion, which work in opposite directions, lead to the extinction of well-known iconic companies. Such implications to organizations were nicely analyzed in a paper written by Nassim Taleb, in which he shows how the Prospect Theory payoff curve is convex and therefore fragile. His analysis shows that if all you do is focus on small gains in your strategy, your payoff is likely to be negative in the long run, reflecting the strategy adopted by incumbents like those who went bankrupt. Taleb goes deeper into why such decision-making is fragile in his best-selling book Antifragile.

The decision-making process is due to the operating systems at work in our brains, and it’s what Kahneman refers to as System 1 and System 2, where System 1 is the lizard-thinking brain or intuition. System 2 is the analytical method of thinking that requires attention and effort to analyze all our available choices.

Our brain engages System 1, or unconscious thinking, far more often in this day and age than we would want it to. When humans lived in caves, System 1 operated mainly in the presence of threats. Fast-forward to today, and System 1 engages at every juncture or challenge you face during a normal day at work. Be it when you’re having a difficult conversation with an employee or when you’re dealing with a situation that requires instant decision-making or simply when processing new information, like, for example, what you’re watching and doing right now. If your first instinct was to view this information with skepticism, that’s perfectly normal, and it’s simply because our brains have to exert energy to connect the dots. They have to process new information commonly perceived as a threat nowadays. Our world is plagued with fake news and scams, so our brain will trigger System 1 when we encounter new information, whether we like it or not.

Well-trained leaders and experienced professionals do not let System 1 take over at will, but it does require effort, discipline, and training. Now, more than ever, our workdays are loaded with new information, emergencies, and constant challenges, all of which require spontaneous decision-making. Making matters worse, due to data overload, the data designed to help us make the right decisions during such instances are either too complex, insufficient, or inadequate for helping us make the optimal decision when we desperately need to.

So how do you tackle this paradox? First, it would help if you narrowed your focus when processing new information by sifting through it quickly and zooming in on what really matters to make the right decisions without bias; an approach that can be adopted is called Systems Thinking. Systems Thinking is needed when your situation or case is in a nonlinear setting or where Power Law distributions apply.

One approach to managing the paradox that we’ve applied successfully on dozens of organizations works by leveraging collective intelligence in some areas while retaining processes and control in other areas that require it. It minimizes the trade-off between collective intelligence that can be achieved from individuals and the influence of group leaders, then dampens it where and when augmented intelligence is needed most.

References

Harding, D., Vorobyov, A., Kumar, S., & Galligan, S. (2022, February 8). State of the M&A Market. Bain. https://www.bain.com/insights/state-of-the-market-m-and-a-report-2022/

Kahneman, D. (2011). Thinking, Fast and Slow. Farrar, Straus and Giroux.

Kengelbach, J., Utzerath, D., Kaserer, C., & Schatt, S. (2010, March 27). How Successful M&A Deals Split the Synergies. BCG Global. https://www.bcg.com/publications/2013/mergers-acquisitions-postmerger-integration-divide-conquer-deals-split-synergies

Kohnová, L., & Salajová, N. (2019, June). (PDF) Industrial Revolutions and their impact on managerial practice: Learning from the past. ResearchGate. https://www.researchgate.net/publication/334016615_Industrial_Revolutions_and_their_impact_on_managerial_practice_Learning_from_the_past

Martin, R. L. (2016, June). M&A: The One Thing You Need to Get Right. Harvard Business Review. https://hbr.org/2016/06/ma-the-one-thing-you-need-to-get-right

Merger Review. (n.d.). Federal Trade Commission. https://www.ftc.gov/news-events/media-resources/mergers-and-competition/merger-review

Miles, L., Borchert, A., & Ramanathan, A. E. (2014, August 13). Why Some Merging Companies Become Synergy Overachievers. Bain & Company. https://www.bain.com/insights/why-some-merging-companies-become-synergy-overachievers

Morey, T., Forbath, T., & Schoop, A. (2015, October 11). Customer Data: Designing for Transparency and Trust. Harvard Business Review. https://hbr.org/2015/05/customer-data-designing-for-transparency-and-trust

Post-Merger Integration. (n.d.). BCG Global. https://www.bcg.com/capabilities/mergers-acquisitions-transactions-pmi/post-merger-integration

Systems Thinking — Rethink Everything. (2022, January 13). Systems Innovation. https://www.systemsinnovation.io/post/systems-thinking-rethink-everything

Taleb, N. (2010). Convexity, Robustness, and Model Error inside the Fourth Quadrant. https://www.fooledbyrandomness.com/OxfordBTLecture.pdf

Taleb, N. N. (2012). Antifragile. Random House (US) Penguin Books (UK).

Thompson, E. K., & Kim, C. (2020). Post-M&A Performance and Failure: Implications of Time until Deal Completion. Sustainability, 12(7), 2999. https://doi.org/10.3390/su12072999

Value of mergers and acquisition (M&A) transactions worldwide from 2010 to 2021. (2019). Statista; Statista. https://www.statista.com/statistics/267369/volume-of-mergers-and-acquisitions-worldwide/